Background

In 2015, the Federal Government of Nigeria approved the sum of $2.1bn1 to provide intervention package to help bankrupt states in Nigeria pay salaries. While there has been increasing agitation for2 and against3 resource control, not much attention has been given to public finance management practices and accountability mechanisms in state and local levels.

Public audit no doubt plays significant role in improving government’s spending and revenue capacity by limiting fiscal behaviors that result in waste, misallocation or misappropriation and corruption. It is important to recognize the impact of sub-national audit which is aimed at strengthening public finance management and accountability structures at state and local levels as is the practice at the national.

Sub-national audit and other public finance accountability measures are not only crucial for good governance and development but particularly important to fiscal health condition of state and local governments. The inability of public audit to yield intended benefit as provided for in section 125 of the 1999 constitution as amended cannot be separated from the maximum control of the executive arm over the legislature and judiciary at sub-national level. It is therefore important to allow democratic institutions at state and local levels to function effectively so that public resources can be adequately accounted for.

Objective

The objective of SAE index 2020 is to assess the level of transparency and accountability operational in the management of public funds in all 36 states of the federation of Nigeria through the lens of public audit and key actors in the public audit cycle. While the methodology and scoring criteria adopted in this assessment has been very objective and dependent on publicly available information, PLSI commits to continuous review of its methodology and scoring criteria.

The SAE index 2020 is an attempt to forge healthy competition to foster accountability in the management of public resources at sub-national level and states now have the opportunity to optimize their financial management practices and improve on their accountability structures.

Context

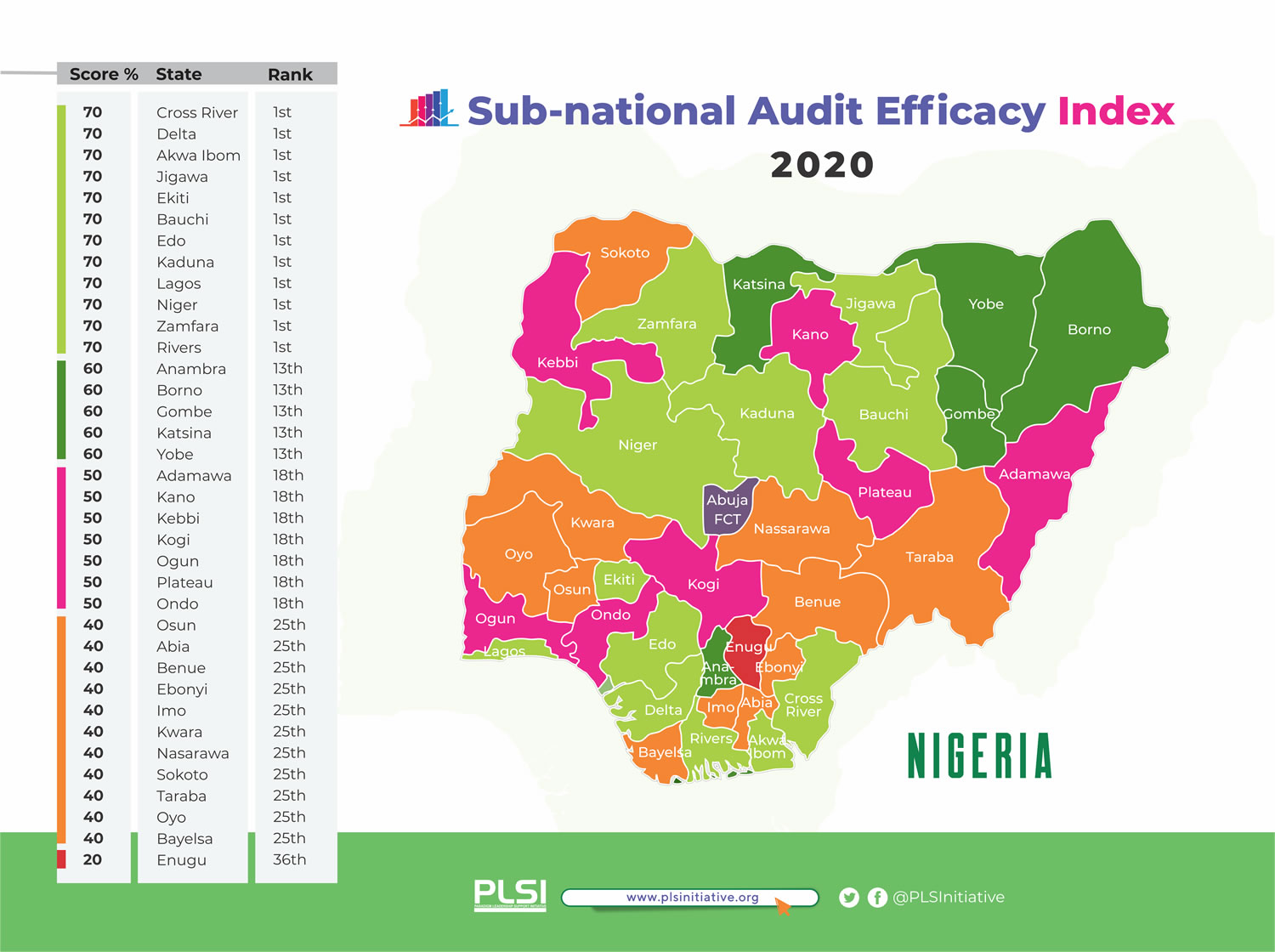

Although there is significant room for improvement, SAE index 2020 ranks twelve states including Delta, Jigawa, Kaduna, Lagos, Niger, and Rivers as states with the most potent audit process in Nigeria having scored 70/100. Also, Anambra, Borno, Yobe, Katsina and Gombe occupied 13th position with 60/100 as their score while the 2020 index ranked Oyo, Sokoto, Imo, Benue among others 25th with 40% score point and Enugu as state with the least potent audit mechanisms having score 20/100 and ranked 36th.

Conclusion

The lack of independence of Legislative arm of government at sub-national level is a cause for concern and this is evident by the recent call for legislative and judicial autonomy4 across the 36 States of the federation. The inability of State Assemblies’ Public Accounts Committees (PACs) to issue recommendations based on their review of Auditor-General’s report is negatively impacting the public audit eco-system particularly at the sub-national level which is in turn hindering accountability in the management of public funds.

Similarly, the failure on the part of sub-national audit institutions to allow for citizens’ participation in the audit process renders audit functions inadequate and unable to facilitate sustainable development. It is disappointing to know that 50% of the states including Sokoto, Imo, Osun, Benue, and Anambra do not have modern audit laws that should guarantee independence of the Auditor-General in their states and enhance effective stakeholder involvement in their states’ audit process. Some states including Zamfara, Delta, Kano and Edo are however showing progress having enacted modern audit laws and should be encouraged to do more. Also, Delta state is among the very few if not the only state that has published audit report on Covid-19 intervention.